Contents

There are 4 issues that it’s essential specify whenever you wish to purchase or promote an choice contract:

The underlying asset

The kind of choice: put choice or name choice

The choice expiration date, and typically time, as a result of some expiration dates have settlement time on the open (AM expiration) and on the shut (PM expiration).

The strike worth

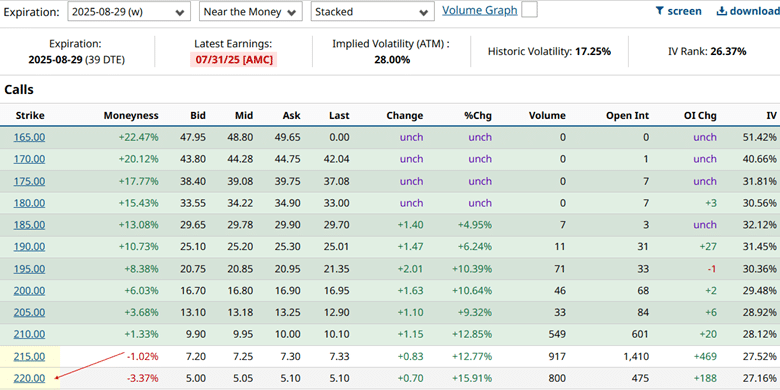

For instance, the beneath choice chain reveals the decision choices (choice kind) for the Apple inventory (the underlying) that’s expiring on August 29, 2025 (expiration date).

Specifically, I’m trying on the name choice with the strike worth of $220 (the one pointed to by the purple arrow). And I’m taking a look at it on July 21, 2025.

Now that I’ve pinpointed the precise choice contract of curiosity, I can see some choice metrics with this specific contract.

Many platforms offers you these metrics.

However we will likely be utilizing Barchart at present, which you’ll be able to see within the above screenshot.

Quantity

Variety of contracts traded at present.

Open Curiosity (OI)

Complete variety of contracts at the moment open.

Bid Ask Unfold

That is the distinction between the value at which patrons are “bidding” to purchase the choice and the “asking” worth that sellers want to promote.

Subsequently, the bid worth is all the time lower than the ask worth as a result of patrons wish to purchase low and sellers wish to promote excessive.

The distinction between these two costs tells us in regards to the liquidity of the choice.

The extra liquid, the narrower the bid-ask unfold.

The tighter the bid-ask unfold, the decrease the price for coming into and exiting the choice contract, as a result of one would lose much less to “slippage” as the value of the choice fluctuates between the bid and the ask worth.

The mid-price is the value that’s proper within the center between the bid worth and the ask worth.

Sometimes, when quantity and open curiosity are increased, the bid-ask unfold is tighter.

Implied Volatility (IV)

Implied volatility is the market’s forecast of future volatility based mostly on choice pricing.

The above screenshot reveals that the 220-strike contract has an IV of 27.16%.

Because the IV doesn’t range an excessive amount of whether or not we go up or down just a few strikes, Barchart additionally offers the final volatility metrics for the ATM (at-the-money) strikes for the August twenty ninth expiration within the header as an Implied Volatility of usually 28%.

This volatility implies that AAPL is predicted to maneuver 28% up or down yearly.

IV Rank

Some shares have a tendency to maneuver quite a bit (excessive volatility) and others much less so.

Is an IV of 28% excessive or low for AAPL inventory?

The IV Rank tells us the place the present IV sits in relation to the previous yr’s vary.

Proper now, the IV Rank is exhibiting 26.37%, which implies that it’s close to the underside quarter of its IV vary.

Historic Volatility

Historic volatility is how a lot the inventory moved on an annual foundation, versus IV, which is the projected motion.

Moneyness

This tells us whether or not this strike of our choice contract is in-the-money, out-of-the-money, or at-the-money.

If the strike worth is near the present market worth of the inventory, then we are saying that the strike is at-the-money.

Since AAPL’s present worth is $212, the $220 strike for the decision choice will likely be out-of-the-money.

A name choice is out-of-the-money when its strike worth is above the present inventory worth, as a result of there isn’t any worth if we had been to train the contract now.

This name choice offers us the proper to purchase AAPL at $220.

No use shopping for at $220 when AAPL is buying and selling at $212.

This name choice has no intrinsic worth proper now.

But it surely does have extrinsic worth, as a result of somebody is prepared to purchase the choice at $5.05 per share.

Extrinsic worth is the worth of chance – the chance that it might turn out to be worthwhile sooner or later.

Some informally consult with extrinsic worth as time worth.

How far in or out of the cash is moneyness? Barchart reveals that this name contract has a moneyness of -3.37%.

Unfavorable worth means out-of-the-money.

The 200-strike would have a moneyness of 6%.

This strike is within the cash as a result of this name choice permits us to purchase AAPL at $200 per share, whereas it’s buying and selling at $212 per share.

It has an intrinsic worth of $12 per share.

Take into account that we had been solely speaking about name choices.

Put choices are totally different.

They’re out-of-the-money when the strike worth is beneath the present inventory worth.

Break-even worth

If we had purchased this name choice on the mid-price of $5.05 per share, spending $505 to purchase the contract (which represents 100 shares), then what worth AAPL must be at expiration for us to be worthwhile shopping for this selection?

AAPL must be at $225.05.

This is called the break-even worth.

As a result of if AAPL is at $225.05 at expiration on August 29, we are able to train the $220-strike choice and purchase AAPL at $220 per share, profiting $5.05 per share.

Since one contract permits us to do that for 100 shares, we acquire $505 from the train, which is simply sufficient to cowl our preliminary value of the decision choice. We break even.

Chance of revenue

That is the chance that the choice will likely be worthwhile at expiration.

What are the probabilities that AAPL will get to $225.05 at expiration?

That relies on how far out-of-the-money the choice is correct now.

It additionally relies on the IV of the inventory (how a lot AAPL can transfer).

Different software program applications could possibly calculate the chance of revenue extra precisely. However as a tough approximation, we are able to use Delta as a proxy.

Free Lined Name Course

Delta

It seems that the Delta on the choice chain will roughly let you know how probably it’s for the choice to get within the cash.

For our name choice to be worthwhile, the choice must first get in-the-money, after which AAPL has to maneuver additional as much as obtain sufficient good points to additionally cowl the preliminary value of the choice.

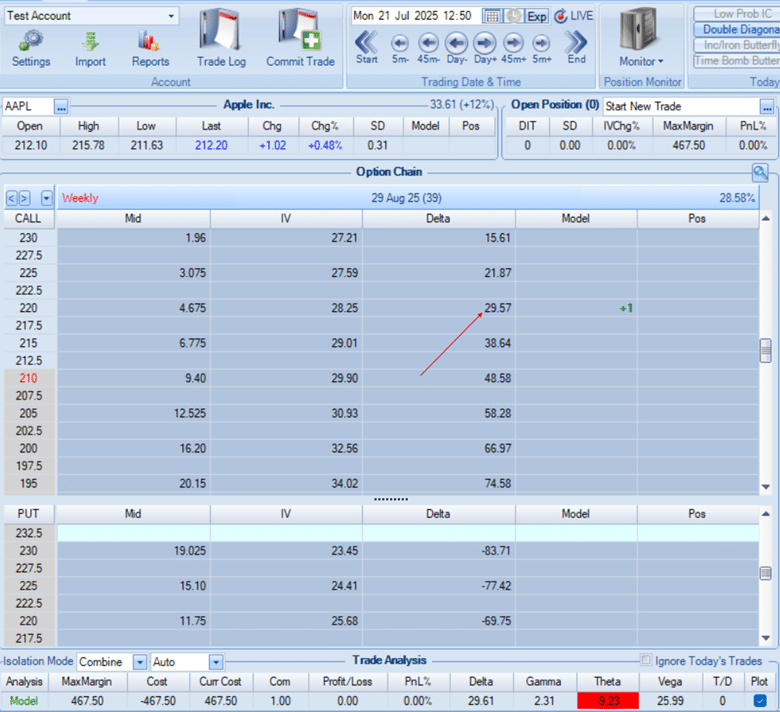

In OptionNet Explorer, we see that the decision choice has a delta of 29.57. We simply say that it’s on the 30-delta.

Which means that there’s a 30% likelihood that our name choice will likely be within the cash at expiration.

There’s a 30% likelihood that AAPL can transfer up from $212 to $220 at expiration.

Then it wants to maneuver up one other $5.05 to cowl the preliminary value of the choice.

Within the OptionNet Explorer commerce evaluation panel on the backside, we additionally see one other Delta of 29.61.

For a single choice, these two Deltas will likely be primarily the identical.

Delta is a Greek that measures how a lot the value of an choice is predicted to vary for a $1 transfer within the underlying.

That is its main definition.

It tells the directionality of the choice.

If its worth is constructive, then we would like the underlying to maneuver up in worth in order that the choice worth will increase.

If its worth is detrimental, then we would like the underlying worth (AAPL worth) to maneuver all the way down to revenue from the choice.

The magnitude of the worth of Delta tells us how directional the choice is.

Theta

Within the commerce evaluation panel, we additionally see that this name choice has a theta of -9.23.

Which means the worth of this selection loses cash as time passes, with all different issues being equal.

If theta had been constructive, the choice place would enhance in worth because it will get nearer to expiration, with all different issues being equal.

Vega

Vega is a Greek that tells how delicate an choice is to implied volatility.

If Vega is constructive (as on this case of +25.99), the choice will enhance in worth if IV will increase.

If Vega is detrimental, the choice place will lose worth as IV will increase – ceteris paribus.

Ceteris paribus is only a Geeky time period utilized in economics to imply assuming all different elements keep the identical in order that we are able to isolate the impact of 1 variable.

Rho

Together with Delta, Theta, and Vega, Rho is the fourth choice Greek (and is the least vital). It tells how a lot the value of an choice adjustments for a 1% change within the risk-free rate of interest.

Gamma

There are additionally second-order choice Greeks.

We’d like not fear about them, besides maybe for Gamma. Gamma measures how a lot the Delta of an choice will change when the underlying inventory worth strikes by $1.

The better the magnitude of Gamma, the extra Delta will change because the underlying asset worth strikes round.

In Conclusion

Suppose all this feels like Greek to you. Don’t fear.

It may be complicated if that is the primary time you will have heard of all these phrases.

And we’ve lined lots of choices metrics at present.

Bookmark this web page to be able to re-read it later, and ultimately you’ll come to see how all of the items are associated.

We hope you loved this text on choices buying and selling metrics.

When you’ve got any questions, ship an e mail or go away a remark beneath.

Get Your Free Put Promoting Calculator

Commerce secure!

Disclaimer: The knowledge above is for instructional functions solely and shouldn’t be handled as funding recommendation. The technique introduced wouldn’t be appropriate for traders who usually are not accustomed to alternate traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.